The individual insurance market in the United States has always been a funny beast. One part of the market has always been a market for long term insurance for freelancers and very small businesses. In this part of the market, people could reasonably assume that they want to stay with a single insurer and in a single network for several years. And if their lives changed, they just called their insurance agent to make a change to their policy. They could add their baby, their new spouse, drop their 19 year old college student who is now covered by their college’s insurance. This is true both pre and post-PPACA.

The other side of the individual market is very different. It is a very high churn market. 40% to 50% of the people in the individual market are in the market for under a year pre-PPACA. That is because the individual health insurance market is a holding tank until something better comes along. That something better is often employer sponsored coverage or Medicare or CHIP or the VA. The something better could be from age (Medicare), eligibility processing for CHIP ( side note, CHIP is awesome, better than Platinum coverage), new employment or getting on someone else’s insurance at their job.

When I was laid-off early in my career, I had an individual policy with an $8,000 deductible. I stopped that policy the moment my benefits started at Mayhew Insurance. This is common for the individual market.

The individual market changed dramatically with PPACA. Instead of being a medically underwritten, cherry picking market, it became a guaranteed issue market. However it is still a holding pattern for a lot of people. If someone is single and makes between 200% and 300% of the Federal Poverty Line odds are that if they are offered employer sponsored coverage at work, the employer sponsored coverage will be as good or better than what that person can afford on Exchange and the visible premium will be less. If that person makes over 300%, odds are strongly in favor that employer offered covered is superior to affordable Exchange coverage in most markets. People who earn under 150% FPL will see lower deductibles and lower premiums on Exchange than on most employer sponsored plans.

So people on Exchange are still looking for something better and ESI can be better for a lot of people.

That leads to an incentive structure for people who know that they have high cost needs and have a highly probable short term special enrollment window coming up (changing jobs, marriage, major cross country move) to get a high actuarial value policy (Platinum for instance), max out the benefits and get a lot of expensive things done before the special enrollment window.

Michael Hiltzik at the LA Times looks at this issue as some of the anti-PPACA hacks are at it again claiming that the Special Enrollment Periods are leading to significant gaming of the risk pools.

These remarks set the hearts of some members of the Obamacare deathwatch aflutter. Bloomberg’s Megan McArdle speculated that on the possibility of gaming by customers, though she later owned up via Twitter to being “sort of skeptical” that such strategies were widespread.

Cato Institute’s Michael Cannon, however, declared in Forbes that such “free-riding,” which poses “a serious threat to Obamacare’s future,” has now been established as “a real problem.”…

One insurer has provided numbers. Iowa’s Wellmark says 135 members signed up, got treatments, and then dropped their coverage after running up sizable bills. But they were about one-tenth of one percent of an individual insurance pool that appears to be about 150,000 members.

Is this first surprising and secondly a problem?

This should not have been surprising. Insurance companies going into Exchange had good experience with a similar guarantee issue program with uncertain contract lengths. That program is COBRA. COBRA has historically had an incredibly sick population compared to the same employer group’s currently employed population. The COBRA population was incredibly sick because COBRA was expensive as hell and the insured member had to pay the full cost of premium plus administrative fees.

When I was laid off early in my career, I had coverage that probably was between 85% and 90% actuarial value from my previous employer. I paid $75 a month for that coverage. My COBRA letter stated that if I wanted to enroll in COBRA, I would need to send $900 a month for individual coverage. My former employer had several people with MS, a few cancer survivors, and a family with a child with cystic fibrosis. It was an ugly risk pool. I was in my mid-20s and healthy as a horse. I could not afford to sign away half of my monthly unemployment insurance for medical insurance. At the same time, another colleague who was laid off in the same round went on COBRA as she was in fighting cancer and had several chronic conditions. COBRA was a much better deal for her then running naked as she could not get any underwritten insurance.

She found a job seven months later but she had three infusion rounds where the drugs cost $10,000 a round.

Insurers should be able to model (roughly) that there is a lot of movement in and out of the individual market, especially for people who could have better options available. The Exchanges are still data sparse (2017 pricing will be the first year with rich data) but insurers should not be surprised that the Exchange population or at least a subset of it, behaves a bit like COBRA.

Is this a problem?

Not really, and increasingly less so.

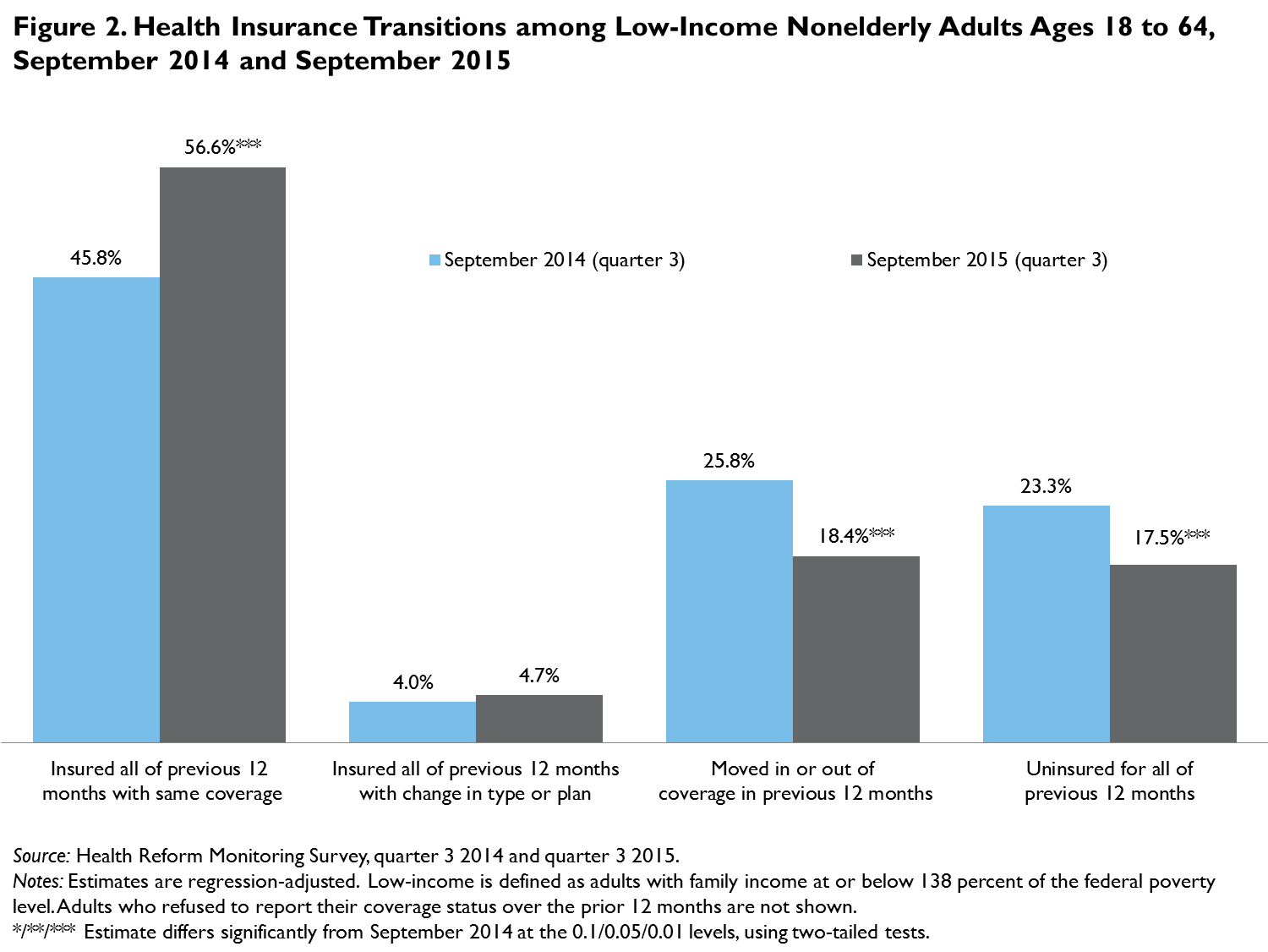

The Urban Institute is showing more people are keeping continuous coverage at a single insurer for the course of a year. There is less churn now than there was a few years ago. Some of that could be related to a better economy and more people having jobs that offer employer sponsored coverage and fewer layoffs. It could mean that the Exchanges are seen as decent coverage all around and moving to different options is not worth the hassle factor.

The Urban Institute is showing more people are keeping continuous coverage at a single insurer for the course of a year. There is less churn now than there was a few years ago. Some of that could be related to a better economy and more people having jobs that offer employer sponsored coverage and fewer layoffs. It could mean that the Exchanges are seen as decent coverage all around and moving to different options is not worth the hassle factor.

More importantly, at most this is a limited actuarial projection problem. Some companies projected this issue better than others, and some did not anticipate it at all. The biggest problem however is that the pricing structure of the Exchange market encourages people to sign up with insurers who have the most aggressively optimistic projections (winners curse), so there could be a lot of year over year churn in the market.

If people are convinced that this is actually a problem, there are a few policy solutions that could happen. The first is advocate and implement single payer. That is not happening until my kids are in college at the earliest.

Secondly, change the nature of the individual qualified health plan market from a month to month market to a year to year market. And if there is a qualifying event, the new insurer and the old insurer pool risk, expenses and costs via a set of back end transfer payments.

This can be an isolated problem, but insurers should have expected some COBRA like behavior in some segments of the individual market as people will move to something better but while they are in a short term product, they will maximize its use value.

dr. bloor

The notion that anything more than a nanosliver of people looking for health insurance have the sophistication to game the market is simply anti-ACA shit-stirring. Most of the friends and clients I know have claimed victory after successfully negotiating the process if they end up with something, anything.

Like healthcare consumers who will comparison shop for anything more pressing than an elective vasectomy, they exist only in Econ textbooks and nowhere in nature.

Richard Mayhew

@dr. bloor: Agreed, there is a sliver of people who are looking for an angle, and in my opinion, it is not a big deal, the insurers should have been able to project this type of game fairly well based on COBRA experience.

Benw

I stand, fists and jaws clenched, as my face is bathed in tears, who will speak for the poor insurance companies? WHO WILL SPEAK FOR THEM!?!

MomSense

The insurance companies and providers are the ones who are gaming the system. The whole system of co-pays and deductibles seems to be designed to discourage people from availing themselves of services. And heaven help you if you want to find out how much a colonoscopy or other screening might cost. Hospitals do not divulge that information and if you can find out approximately how much it might cost, you have to ask specifically if the person who reviews and interprets the test is also an employee of the hospital or do they work for a separate entity. You have to ask because you will get hit with bills from separate entities who are, of course, out of network.

It is damned near impossible to make an informed decision, or be even a remotely good consumer let alone game the insurance market.

Disclaimer: The ACA is a huge improvement and I am happy to have it — but I am really tired of the constant punching down for those of us just trying to access basic medical care.

benw

First, my above snark was directed at the McArdles of the world, not you Richard.

Thirdly and lastly, word to what @MomSense said.

And secondly, this “issue” feels a lot like “voter fraud”, in that (1) it’s very dubious that it’s even happening, and (2) the “solution” is ALWAYS to dismantle something our Republican betters don’t like, like voting access or Obamacare. Bottom line is that the people pushing this BS assume that everything should be a privilege for them and their connected friends to which the rest of us can only aspire. What a fucked up state of mind to think that someone *buying* insurance to use for expensive medical care is some kind of con artist, and not a fellow human being who is sick and needs healthcare.

Healthcare, like the franchise, should be a right.

FlyingToaster

I had private insurance for two years during my 17-year consultancy. It was through a professional group, and was basically “hit by a bus” insurance.

After two years, instead of a 10% increase (expected), they gave me a 50% increase because Massachusetts state law now required them to cover mastectomies and reconstructive surgery. I did not renew, and went bare for 5 years. I never made a claim (they didn’t cover birth control or optical), and was getting most of my care through Planned Parenthood.

I remember arguing with Ted Kennedy at an INC conference about this; I was convinced that the individual mandate would be another cash grab by the insurers. I’ve never been so happy to be proved wrong.

gvg

running up sizable bills might mean they were seriously ill, enough that they might have died rather than what we normally mean by “dropped coverage”. 1/10 th of a % strikes me as a very low number even for deadbeats.

Richard Mayhew

@gvg: Most insurers have a “dead” check box for disenrollment reason, and we can track it fairly easily most of the time as either the death happened under medical care, or someone calls up in a week or two to cancel the premium and presents a death certificate.

BobS

@MomSense: That’s pretty close to what I was thinking while reading the post — McCardle & Cannon are very very upset that very very few people have learned the insurance company playbook well enough to level the field they’re playing on.

Marc

Ah, so we know it’s bullshit then.

burnspbesq

Further to MomSense’s point about obstacles to informed consumer choice, is that what the Gobeille case that was argued before the Supreme Court yesterday is really about?

Richard Mayhew

@MomSense: I completely agree with this statement:

jl

Thanks for all the informative posts.

I think any insurance market without some well defined risk pool, and an exogenous mechanism to qualify people for that risk pool is a funny beast because it is inherently unstable. This has been known since the famous Stiglitz-Rothschild research back in the 1970s. Defining the risk pool is very difficult in health insurance because the cost structure of health care is not easily separable across time. And the costs of market failure are very high because they concern death and disability, which are costly and not fungible, and few or no substitutes (compared to say, car insurance, or property insurance). And government support for those who lose in the market failures is skimpy compared to say, flood and earthquake insurance). Anyway, there are fixes that work for other insurance markets, but they don’t work well with health care.

So, I am not surprised that the robot’s breakfast of metals that is susceptible to gaming is in fact being gamed. I think RM makes a good point about how important this kind of consumer gaming is. Even though the consumers can game it, there are limits on how much insurers can do to take advantage of the consumer gaming, and it is the joint efforts of both that slowly destroy the market’s ability to pool risk.

The standard solution in other countries that have not adopted a national health care service is to define the risk pool by enforcing a uniform basic insurance policy that must be offered to everyone, with well defined limits on price differentials by age. People who want more or customized coverage can by that on a separate, much less regulated, supplemental insurance market.

The current system is much better than the old one, but it could be better.

RaflW

@Benw: Harry and Louise.

@Marc: I think we can even take out the word speculated and your statement holds.

RaflW

momsense going off about invisible pricing is spot on. I’m not really sure how copays and co-insurance are really supposed to help us make care choice decisions when we don’t know what prices are.

That’s a major problem that needs to be addressed. And it won’t be, as long as we have 41 or more GOP Senators, I fear.

Julia Grey

I just got done helping my son get a new individual insurance policy. His previous marketplace insurance company, a co-op, couldn’t keep going here in SC because the risk corridor payment they were entitled to (12.6 percent?) was not enough to support their business. Same thing apparently happened to other insurance companies in the state. They were essentially “run off.” I do not know the structural reasons behind any of that, but I sure would like to.

So now in South Carolina we have a virtual monopoly on the Exchange. All but one (?) of the “Silver” plans are Blue Cross-Blue Shield, and differ only in the varied ways they can avoid paying out for medical care. You might want to sign up for a $5,000 deductible, say, but you have to meet your entire deductible before you get ANY coverage for so much as an office visit. Or the co-insurance on everything is more than 50% even after your deductible is met, stuff like that. Figuring all that out was a nightmare.

My son’s income is going up this year in a new job, so he’ll make about $31,000, and will therefore get the princely sum of $30 a month in premium subsidy, but of course, no “extra help” with his deductibles or copays since he’s so rich now.

For the remaining $271 a month in premiums (total for the year $3252–MORE THAN 10% OF HIS INCOME–what happened to that 9.5% “affordability” thing?), he gets office visits, generic prescriptions, and in-network urgent care (doc-in-a-box) for relatively reasonable co-pays that he can come up with from his pocket and hand across the counter on any given day ($25, $60, etc). Yay. He’s coughing up that three grand for the privilege of not being charged full “uninsured patient” prices when he goes to the doctor.

EVERYTHING else, including lab work, x rays, emergency room, etc., is subject to his $6850 deductible, which is also his max out of pocket. So he’s essentially naked, and will only benefit from this insurance if he has a huge event that exceeds his deductible. It’s catastrophic insurance with a small side benefit.

Okay, you say, it was ever thus. People in mid-level insurance policies always had to pay deductibles in addition to their premiums before their insurance “really” kicked in (and paid PART of their bills). But maybe it’s just the double whammy of his increase in income and his insurance co-op going belly up, but the deductibles on these BC-BS MONOPOLY policies offered on the exchange seem really excessive this year. Or am I imagining things, and this is all perfectly reasonable because he’s making more money this year?

HOWEVER! If he should by chance screw up and allow a non-network provider to do anything for him, in any facility, whether he is awake or asleep, or is directed to an out-of-network lab or imaging center, none of that expense goes against his deductible, and he has to pay whatever is billed. The hidden price/conspiracy of silence is especially infuriating under these circumstances.

Oh, and one of the most prominent gaps in this stellar coverage? The world-class teaching hospital here is “out of network.”

Okay, rant over. But I had to scream to someone!

jl

@RaflW: I think our ACA system is a poor approximation to the Swiss and Dutch approach, and policies to ensure much more price transparency is a big part of the Swiss system. And IMHO, lack of price transparency is causing problems with the Dutch system.

Tissue Thin Pseudonym

Richard, if you’re still reading this thread, is there anywhere to go to find clear and simple information on what my options are if my employer offers a really crappy health plan? Honestly, the information on the one my employer offers makes it sound like it couldn’t possibly meet the minimum standards set by the ACA, but that may just be because the description is completely opaque, and may be because they don’t really want us to sign up for it. But I’d like to know what my outside choices are.

J R in WV

One tenth of one percent – or in other characters, .001

One thousandth of the population. That is about the same percentage of welfare recipients being drug tested who show positive for recreational drug use, at least around the same magnitude IIRC. So this is obviously an emergency that threatens the foundations of America, and we need to stop the ACA before it is too late to fix things!!

Ask any Republican legislator!! They are out there trying to kill people by repealing health insurance, because, AMERICA, hate, hatefulness. Yet people who’s lives depend on the ACA vote for Republicans who vow to remove their health insurance, dooming people to lingering death from kidney failure, or cancer, or, or, or….

People are crazy.

Thanks, Richard, for the time you invest in our education!

I have run into the “How much will it cost?” “Huh? We don’t know!” predicament myself. It isn’t any fun at all !!