The Commonwealth Fund has a new issue brief regarding what happens when large insurers merge.

TLDR: The social surplus went from providers getting hookers and blow to insurers getting hookers and blow. No public consumption of hookers and blow.

It is making me change my thoughts on a couple of things.

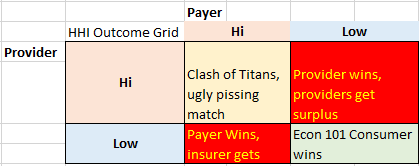

My previous model was a fairly simple 2×2 grid analysis of relative market power between payers and providers.

If we take a ratio of the Provider GINI Ratio to the Payer GINI Ratio, we can make some strong inferences about how the local health insurance market works and where relative prices lie.

If the ratio of ratios is close to one, the providers and payers are evenly matched. If the ratio is significantly above one, providers have a market power advantage as the largest provider groups control a significant chunk of sub-markets that the payers need access to. If the ratio is significantly below one, the payers have market power. They can pressure providers to take low rates.

This thought process leads to the grid on the left. That grid supports an  analysis that suggests that supporting some insurance company consolidation in the face of provider consolidation is a second best outcome for the public. I had been thinking that markets where providers are fairly concentrated and insurers are comparatively fragmented a movement towards a Hi-Hi concentrated would consume signifcant social rents while spilling off some social surplus that had been previously extracted by the dominant providers back to the public.

analysis that suggests that supporting some insurance company consolidation in the face of provider consolidation is a second best outcome for the public. I had been thinking that markets where providers are fairly concentrated and insurers are comparatively fragmented a movement towards a Hi-Hi concentrated would consume signifcant social rents while spilling off some social surplus that had been previously extracted by the dominant providers back to the public.

There are two problems with this idea.

The first is from a recent speech by Assistant Attorney General Bill Baer on anti-trust enforcement:

We have also seen attempts to justify mergers on the ground that they will improve a company’s negotiating position. Hospitals want to merge to get leverage over a dominant insurer; insurers want to merge to get leverage over a dominant hospital. Courts have long rejected the notion that “countervailing market power” justifies anticompetitive mergers or agreements. It is not at all clear that consumers win where a merger is justified solely on creating more bargaining leverage, the so-called “second 800 pound gorilla defense.” As my friend and mentor Bob Pitofsky said about this argument some years ago, the antitrust laws “reflect a fundamental premise that consumer choice, rather than the collective judgment of sellers, should determine the mix of price and quality options available in the market place.” This is still true. Consumers do not benefit when sellers – or buyers – merge simply to gain bargaining leverage. Consumers benefit when there is entry, expansion, innovation and competition.

So my model violates current federal policy. That is one major strike against it.

The second major problem with my simplified model is that it does not work. The Commonwealth Foundation’s brief shows that there is no net new distribution of social surplus to consumers.

Studies of hospital price and insurance HHI, which use different data sources and look at different time periods, generally find hospital prices are lower in geographic areas with higher levels of HHI—that is, where there is higher insurance market concentration. This relationship also holds when researchers study changes over time: in markets that are becoming more concentrated, there is slower growth in hospital prices. But lower prices for health care services will benefit consumers only if they are ultimately passed through to consumers, in the form of lower insurance premiums or out-of-pocket charges….

Several studies document lower insurance premiums in areas with more insurers. These studies span a variety of segments, including the public health insurance marketplaces, the large-group market (selfinsured and fully insured plans combined), and Medicare Advantage.18,19,20 One recent study suggests premiums for self-insured employers are lower where insurer concentration is higher, but premiums for fully insured employers are higher.21 The best available evidence on the impact of consolidation comes from what are known as “event studies” or “merger retrospectives,” such as the aforementioned Aetna–Prudential merger study. The researchers on that study found that premiums (for a pooled sample of self-insured and fully insured large-group plans) increased significantly more in areas with greater pre-merger market overlap. Moreover, the premium increase was not limited to the merging insurers; rival insurers raised premiums as well (in areas where the merging firms had substantial overlap). This is particularly notable in light of the fact that following the Aetna–Prudential merger, health care employment and wages were reduced. The cost savings were not passed on to consumers.

I had previously thought the major insurer mergers would probably be approved with minor divestitures in regions where the combined entities were the overwhelmingly dominant players. I think I am wrong on that thought.

I think my model is a decent little micro model of how pricing is determined within a single market segment/region at the current point in time. But as I expanded it to encompass a much larger space, the model keeps on running into reality. Reality will eventually win. I am not sure what will replace my macro mental model yet.

Baud

Since when has that ever stopped anyone?

Richard Mayhew

@Baud: I would like to maintain my own internal self-image as part of a liberal/left technocratic wonk community. It is a tribal marker that we occasionally examine our models for too notable divergences from reality. So this is not an empirical post but a cognitive dissonance minimization and tribal affiliation maintenance post if that makes it easier for you :)

Baud

@Richard Mayhew:

Seems easier just to blame Obama when the models don’t work. But whatever floats your boat.

Richard Mayhew

@Baud: that works too

pluky

How I wish that the SOA would recognize these posts as valid sources of CPE credit. They are so much better than a lot of the authorized drivel.

Fred Fnord

It’s kind of like if copper pipe were made by only one company, who therefore could charge monopoly pricing, and could force the price of copper down by playing one provider off against another. And we decided to fix the problem by allowing all the copper mines to be owned by the same company.

piratedan7

the house always wins, the consumer almost never does…

max

I had been thinking that markets where providers are fairly concentrated and insurers are comparatively fragmented a movement towards a Hi-Hi concentrated would consume signifcant social rents while spilling off some social surplus that had been previously extracted by the dominant providers back to the public.

I don’t see how the model can work. There’s an provider to insurer market, where the profits go to whomever comes out ahead, and an insurer to consumer market, where the insurers use their market power to charge as much as they can get away with and never the twain shall meet.

I don’t see a transmission mechanism to insured consumers (since they might have to choose and they seem to be bad at this, what with being sick and all) from either the insurer wedge or the provider wedge. Perhaps if the providers are highly profitable, the will provide better services for a given amount of money, and if the insurers are successful, they will keep rates from rising too fast, but there’s no ‘driving you out of business for not providing your services well’ and no ‘you can become more profitable by providing better services for less’ mechanism of consumer choice.

max

[‘I can see how it would reduce the bleeding from increasing costs to the government though.’]

Mnemosyne (tablet)

I was very surprised at Thanksgiving to hear my Reagan-worshipping brother voluntarily say that there may be at least some parts of healthcare that are necessary but unprofitable, so the government should run those. My jaw is still a little loose from that.

(The specific topic at hand was home infusion, FWIW. Very necessary for people on long-term therapies and it saves the whole system money since it cuts down on hospital admissions, but not a profit-generating enterprise.)