As open enrollment approaches, we’ll see a flurry of three letter acronyms thrown at us. To insiders and daily users of this information, a PPO HDHP embedded 500/1500/20% makes perfect sense as a way to express a lot of information in a condensed, understandable fashion. To anyone else, that is gibberish. There are two basic interacting elements of the jargon that people have to wade through. The first is plan design. This is based on two sets of questions. Do people have to go through their primary care provider (PCP) as a gatekeeper for higher level care, and are there out of network benefits? The other is benefit design which means how much does each party pay, when, and to what limit? These two factors next hook to a network which leads to pricing decisions.

Very different plan designs can be attached to a single benefit design structure. Those pairing can then be hooked to multiple networks. A PPO 500/1500/20% attached to Mayhew Broad will price out much higher than an HMO 500/1500/20% that is attached to Mayhew Super Narrow. PPO 500/1500/20% Broad will also price out higher than HMO 500/1500/20% Broad.

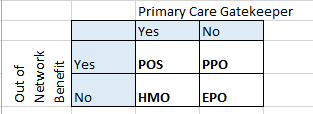

Today we’ll just look at the most basic plan design elements. It is a 2×2 grid.

Point of Service (POS) is an odd bird. It is sold, but not widely. People are required to go through their PCP for higher level care. This is a utilization management/minimization strategy but it allows significant leakage outside of the network. Out of network benefits will usually have twice the deductible and out of pocket maximum as well as a higher percentage of co-insurance than in-network benefits, but the insurer will pay once a limit is reached. From the provider side, they can be paid at either a head payment (capitation) with health management risk transferred to the provider or on a fee for service basis where the insurer keeps the health risk.

Health Maitenance Organizations (HMO) require primary care providers to manage care. The PCP authorizes higher end care and they are expected to say no a lot more in a pure HMO arrangement than other plan designs as payments are structured as a risk adjusted monthly payment per person. If the provider group spends less than the average monthly payment, they make money, if they spend more, they lose money. The goal is to encourage cost effective care (ie physical therapy for back pain before considering surgery). Benefits are restricted to in-network providers only. Leaving the network for routine care may have the bills reduced to a percentage of usual and customary rates (UCR) instead of the absurd initial ask of a provider, but the insurer will not pay anything of that percentage of UCR. Sometimes there will be no reduction from the initial ask. It depends on the insurer and how they have built a wrap-around network to their core network.

Preferred Provider Organizations (PPO) are designs where there are the fewest utilization restrictions. PCPs are not a requirement. If a member is told to get high end specialist care or a surgery, they just have to get on the surgeon’s schedule. The claim will be paid. In network providers will get paid (from a member’s point of view) at a much better rate. There is out of network benefits, although these benefits usually kick in after the member has paid a lot more out of pocket. PPOs became very popular in the late 90s as part of the HMO backlash as they are the anti-HMO. Most PPO payment systems are based on a fee for service model. For a given network and benefit design choice , a PPO plan design tends to be the most expensive as a combination of more optional utilization, and self-selection of people who think they’ll need more care into a PPO design.

Exclusive Provider Organization (EPO) are an in-between step to the HMO and PPO. PCPs are not required (although recommended for most plans). They mostly perform like a PPO as long as person stays within network. If a person wants care, or a provider recommends care, they just have to get an appointment from an in-network provider in most circumstances. The big difference between an EPO and PPO is the out of network benefit. EPOs don’t have routine out of network benefits.

One more note on out of network benefits. The statements on out of network benefits only applies to routine and non-emergency care. If you break a leg two time zones away from your home, or you have a heart attack where the closest hospital is out of network, those claims will be paid up to the point that you are able to be transferred to an in-network provider. If you have Ebola, you probably would be treated at an out of network hospital but those claims would pay as if it was in-network for that particular disease episode.

Punchy

I hate 3 letter acronyms. IMO, they’re confusing. LOL, just kidding. Anyone else excited for the NHL season? And the NFL game tomorrow? ATM, I need Rodgers to get injured. Otherwise I’m losing my PPR league.

Richard Mayhew

@Punchy: WTF, GFY and I am screwed for next week in my league as I have most of the Patriots offense (Brady, Edelman, Gronk) as a high correlation, high scoring machine and they are on bye next week. This strategy has worked for 3 wins so far, but I always knew that the bye week would be ugly. I have Matt Ryan as my back-up QB and then it gets ugly for WR-3/TE as my flex options suck. I figure I can try to trade Ryan in Week 5 (maybe to whomever has Romo or Brees or Rothlesberger — I might take a Ryan for Rothelesberger straight up)

satby

I think the trouble with all of them is trying to figure out if the specialist you were referred to by your Dr is in network. Because I have twice assumed that they were and paid dearly for that assumption.

ruemara

I just want a plan I can afford since I make less than 22k. What the ACA needs is adjustments in subsidy based on COL, or a sensible expansion of Medicare. This year I managed to pay for 3 months of insurance and spent the rest of that time defaulting and using cheaper trauma centers. Instead of the silver, I’m thinking of a PPO bronze. I know you’re doing the Lord’s work in your wonk posts, but this arcanem is beyond me. I just wish the industry was less confusing and expensive.

SP

I feel like the network-only plans are going to see a similar backlash to the ’90s if the shenanigans with out-of-network specialists being called without consent continues. I had minor hand surgery a couple weeks ago, at check-in I asked the account manager if there would be anyone besides my (in-network) surgeon involved and if they would be in-network as well. Her response? “Yeah, I think so.” That’s really reassuring. Turns out it was just the doc and 3 nurses so nothing to worry about (and I also have a very broad plan), but how is it legal for hospitals to hold you liable for charges when they refuse to answer any questions about those charges? Isn’t that a violation of informed consent?

VFX Lurker

I would also like to thank Richard for these informative posts.

For those interested, Covered California offers rate information for 2014, 2015 and 2016. I’m guessing that the 2014-2015 rates are left in there so that people can make note of annual cost increases.

benw

@SP: When a family member had minor surgery last year, the surgeon’s office very dutifully ran all our insurance info and cheerfully told us up front what we had to pay. So far so good, right? Then they sort of mentioned offhand that there would definitely be an anesthesiologist, they couldn’t tell us what the anesthesiologist would charge or if any of it would be in our network, and we couldn’t contact them ahead of time because they didn’t know which anesthesiologist would be available at the hospital the day of the surgery. Total black box. All ended well when our insurance paid the ~$1k anesthesiologist bill after a little teeth-pulling, but come on, guys!

Richard Mayhew

@SP: In most states that is legal. New York and IIRC New Jersey are recently legislating against extortionate out of network chages when procedures are being performed at in-network facilities by in-network main providers. I agree, it violates a common sense understanding of informed consent, but not the legal understanding of that term as most/all hospitals won’t treat non-emergency cases without a signature on a form saying that you’re willing to pay anything that the insurance company won’t pay for.

SP

I’m guessing if I take that form and write something on it about only agreeing to pay charges for in-network providers and only out-of-network providers if first consulted, it wouldn’t be legally binding on them unless they countersigned? Fat chance of that.

richard mayhew

@SP: Not a lawyer, nor do I play one on the internet, but my understanding is that a decent proportion of the fine print on most hospital forms is of dubious enforcability if they are challenged in court BUT the problem of getting it to court is that is more expensive then just paying, and if it looks like it is going to court, the hospital will often drop the charges before actual settlement talks begin.

srv

Is that true of all plan types? I have Kaiser and wonder what happens when I’m out of state. Kaiser is all about your PCP, your care is as good as they are. I presume out-of-network emergencies go to some bureaucrat and not your PCP for review.

Ohio Mom

A little off topic but I just read on another blog that the State of Illinois is not allowing the medical insurance of their university workers to pay for any health care procedures — can this be?

http://clarissasblog.com/2015/09/27/rauner-a-deranged-maniac-on-the-loose/

Richard Mayhew

@srv: It is true. The PCP requirement is for deferrable or elective care. If you are brought into an ER (in network/out of network) with a sucking chest wound or having a stroke or other emergency case, you are getting treated and the claim will be treated (from your point of view) as if you went to an in-network facility.

This applies for all plan designs.

mclaren

This demented gobbledygook is obviously designed to baffle the average person to the point where they make the wrong choice for insurance, then get blamed when their insurance won’t cover their illness.

None of this twaddle makes any difference in any case, since “drive-by doctoring” is guaranteed to bankrupt you if you get seriously ill whatever else happens.

Source: “After Surgery, Surprise $117,000 Medical Bill From Doctor He Didn’t Know,” The New York Times, 20 September 2014.

mclaren

@Richard Mayhew:

This is legally known as a “contract of adhesion” and is illegal.