A common theme that I have seen in comments is that HMO’s will kill people if they are widely adapted.

That is false. Shitty HMOs that are pinching pennies to make next quarter’s numbers will kill people. Shitty PPOs will also kill people while giving them more choices.

Good HMOs are quite possible and they provider very good care.

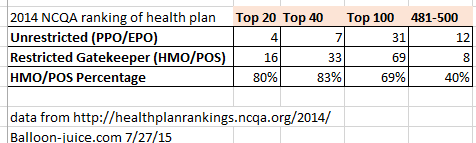

The National Committee on Quality Assurance (NCQA) is the major credentialing and research entity of payers and providers in this country. Health plans work their asses off to look good for NCQA. Some of the requirements are technical (does the web directory show daily hours?), some are mechanical (how many cardiologists per 10,000 members are in each county or within 20 miles etc), and quite a lot of the NCQA scoring system is based on managing basic prevention. How many kids are seeing the dentist in the past year, how many diabetics have received appropriate nutritional counseling, how many lead screenings occurred, how many functional mobility assessments been paid for people with restricted mobility? Health plans work hard to minimize the NCQA gaps and conform to their technical standards.

The 2014 rankings are the most recent rankings out there as the 2015 data cycle is still ongoing. I am rolled up EPO and PPO plans together as they don’t require PCP gatekeepers, while HMO and POS plans do require gatekeepers. I also counted as an HMO plan anything that contained HMO in the NCQA description. Removing that does not change the basic results.

The best plans in the country according to NCQA are overwhelmingly HMO/PCP gatekeeper plans. This not not an artifact of Kaiser. Removing Kaiser from the Top 20 produces 14 plans, or which 10 are non walled garden HMOs.

The best plans in the country according to NCQA are overwhelmingly HMO/PCP gatekeeper plans. This not not an artifact of Kaiser. Removing Kaiser from the Top 20 produces 14 plans, or which 10 are non walled garden HMOs.

Some of this is an artifact of what NCQA measures. Customer satisfaction is only a component of the NCQA score, and PPOs with fewer restrictions usually will score better on customer satisfaction as there are fewer hurdles to jump over. However on the clinical side, the HMOs seem to have better outcomes because the PCP is more involved in patient care.

It is quite possible for an HMO to deliver excellent care, and it is quite possible for an HMO to be completely shitty. The same applies to PPO plan designs. If anything, it is more likely for a PPO to be shitty as setting up a PPO is less involved than setting up an HMO.

Good plans are not dependent on whether or not the a PCP is a required gatekeeper.

Kathleen

I have Humana’s Medicare Advantage HMO coverage, and I’ve been very pleased. It’s kind of a pain to get referrals, but my PCP’s office is very efficient and I’ve been pleased with the specialists PCP provided. It also takes me a little extra time to ensure my provider is in the network, but Humana has never steered me wrong. Most of my care is provided by Tri Health in Cincinnati. I don’t know good the other providers (eg, Mercy) would be.

japa21

I have seen many complaints that by requiring a gatekeeper you are restricting access to specialty care as many PCP’s will try to keep the patient’s rather than refer them on to specialty treatment. The problem with this statement is that it makes two assumptions that may have little basis in fact.

1. Many PCP’s care more about keeping a patient than the quality of patient’s care.

2. Specialty treatment is the preferred option.

Yes, there may be instances of the former taking place as well as, of course, many cases where specialty treatment is the option. But the former would be quite limited and those doctors do get weeded out. And the latter is definitely not always the case.

Part of the reason for creating the gatekeeper concept was that too many people would just go to higher priced specialists for care that could have been handled by the PCP without any referral. And just like there are some PCP’s that may be more concerned with the dollar aspect of keeping patients in the office, there are some specialists that will order unnecessary treatment which results in higher costs all around.

Like any profession, the medical world has its share of unethical and/or incompetents. It doesn’t matter if it is HMO or PPO or the pretty much now defunct indemnity plans. None are perfect and wastefulness and inappropriate care is going to happen in all of them.

And guess what. The same would happen in a single payer environment as well.

raven

Hmm, there are two BCBS of Georgia plans listed and both are pretty bad. I have certainly been charged more for copays this year but the surgery on my hand went well and didn’t cost more than the $200 copay. We do have Kaiser available here now and some people I know have bitched about it. Both are better than the VA I guess.

Steve in the ATL

How about high deductible plans–is there a non-shitty version of those?

My non-expert opinion is “no.”

shell

I know shes talked about the endless rain this weekend, but I hope Betty Cracker is okay with all this flooding in Florida.

PhoenixRising

The problem with HMOs isn’t that the gatekeepers are bad doctors or want to keep the patient in-office when specialty care would lead to better outcomes.

The problem is that there are not always enough gatekeepers. So when members can’t get an appointment to get to the first hurdle within a reasonable time frame, HMOs that don’t meet that particular NCQA metric *are* going to kill people.

In any system that uses PCPs to screen, a lack of competent PCPs taking new patients will result in people dying of curable diseases. That’s the reason for the myth…which now applies to PPOs as well.

Davis X. Machina

@japa21:

Is not the UK’s NHS a nation-scale HMO?

Richard Mayhew

@PhoenixRising: Agreed, not having enough good PCPs is a major problem for mediocre or shitty health plans. And for HMOs, that problem is larger than it is for a similarly shitty PPO.

NCQA has fairly aggressive network requirements (significantly higher in most instances in most states for most specialties than state regulatory requirements) so high scoring HMOs have plenty of PCPs in all counties, while low scoring plans will have bare bones state regulatory access and that will be it.

Gimlet

Here’s an unrelated interesting tidbit of news.

WASHINGTON (AP) — State-run health insurance markets that offer coverage under President Barack Obama’s health law are struggling with high costs and disappointing enrollment. These challenges could lead more of them to turn over operations to the federal government or join forces with other states.

Wonder if this could inadvertently lead to “single-payer” federal government?

Don K

I’ve used an HMO since my working days, and honestly I’ve had no complaints.My biggest problem in seeing specialists is the wait until there’s an open appointment, generally 6-8 weeks in my experience. My PCPs will prescribe treatments, and if those work then that’s that. If not, I’ve never had a problem getting a referral to a specialist. The network is extremely broad, encompassing pretty much every hospital/hospital group in SE MI.

richard mayhew

@Gimlet: Nope, it would just mean more states use Healthcare.gov as setting up the IT infrastructure to run an Exchange is a gigantic PITA.

nanute

Richard,

Any general opinion on EPO’s?

Thanks

Nanute

lahke

I work for the #1 in the country HMO, based in Massachusetts, and you can see that MA plans number large in the list. Part of the reason for this was the move 25+ years ago to guaranteed issue and to forbid recission–at that point, the only workable business model became keeping your members healthy. So we are VERY big on preventive case, disease management, etc. Eventually, the big boys in the rest of the country might figure that out.

Richard Mayhew

@nanute: Roll EPO up into the PPO organizational structure for NCQA purposes.

The big difference between an EPO and PPO is in benefit design. A PPO will pay something for out of network routine services. An EPO will not pay out of network charges for routine services (now if you have Ebola, you’ll most likely be treated out of network at in-network rates).

Within a network, an EPO and PPO are functionally close enough to the same thing for most analytical purposes.

Loneoak

My HMO, Palo Alto Medical Foundation, has a really solid urgent care network baked into their system. The same office where my PCP resides has an urgent care setup that can typically get me/my kid same day care, sometimes even with a drop-in from the PCP. I don’t know any metrics about PAMF’s quality of care, but I’ve never struggled to get attention for my (admittedly non-complicated) medical needs.

Yatsuno

A couple minor points:

The Kaiser plan for WA doesn’t have coverage in the entire state, just in the Vancouver area. This is mostly because of commuters coming up from Portland. I would like it if they would crack up into the Seattle/Spokane areas, as that would cause the other competitors (which I’ll get to in a moment) to start stepping up their game.

The only HMO in WA is Group Health. And they have a bad reputation because they are really only competing against Regence/Premera. But the Blues are actually really good up here, which is why I had a hip replaced with about $1K of out of pocket costs.

? Martin

@Gimlet:

Hmm.

Largest state in the nation is still having a bit of trouble with the subscriber numbers, but the rates are doing okay. 4% is still above inflation, so we’re hardly in the promised land here, but it’s manageable.

Let’s not pretend that the state government doesn’t have a role here. If your elected officials want to see the exchanges fail, then they will fail. CA is a complicated market and yet we can make it work – in part by limiting consolidation so there actually is a functioning marketplace. What’s everyone else’s excuse?

Pseudonymous Bosch

I have an Aetna (Innovation Health) PPO and it blows goats. At least my prior insurance would pay something for the non-preferred equivalent medications (two family members are insulin dependent type 1 diabetics, there are no generic basal or bolus insulins equivalent to what they are using) but these fuckers absolutely refused to pay anything for the originally prescribed medications and insisted both family members switch both insulins to their prefered brands (essentially at the same time — great decision changing two variables at once assholes.) My guess, the preferred brands rate was negatiated contingent on zero coverage for competing brands. Fuckers.

I loathe Aetna/Innovation Health with the passion of a thousand suns.

The Raven on the Hill

Since the OP, more-or-less, a response one of my snarky remarks. I’ll try to gather up my thoughts and state them politely, rather than being snarky.

My text for this sermon is: “‘No one can serve two masters; for a slave will either hate the one and love the other, or be devoted to the one and despise the other. You cannot serve God and wealth.” I see no way a doctor who acts as gatekeeper under employer cost-containment incentives can be anything but ethically compromised.

Still, there are some HMOs that do a pretty good job. Kaiser is a competent one, though it has some problems. Unfortunately, some HMOs do a very poor job. Denial of needed treatment is a real thing, I’ve seen it, and if the disorder not treated is serious, disability or even death can result.

I do not think it would be possible to found an HMO like Kaiser at this time. One would instead get some monstrosity that would manage to be both miserly in doling out care and profligate in the premiums it collects. I’m not sure how that can be managed under the medical loss ratio restrictions in the ACA, but experts are working on it and I have faith in the power of greed. In addition, the ongoing consolidation in health insurance seems likely to lead to a race to the bottom, especially in states which only provide ACA coverage grudgingly.

All of which, Mr. Mayhew, is not meant as a criticism of you; you seem to me both honest and competent. It is also not meant to provide a reason to repeal the ACA, or not to participate. But you aren’t one of the financiers who run this system.