Obamacare’s exchanges go live in three weeks and three days… or as we count time, a gross of coffee spoons.

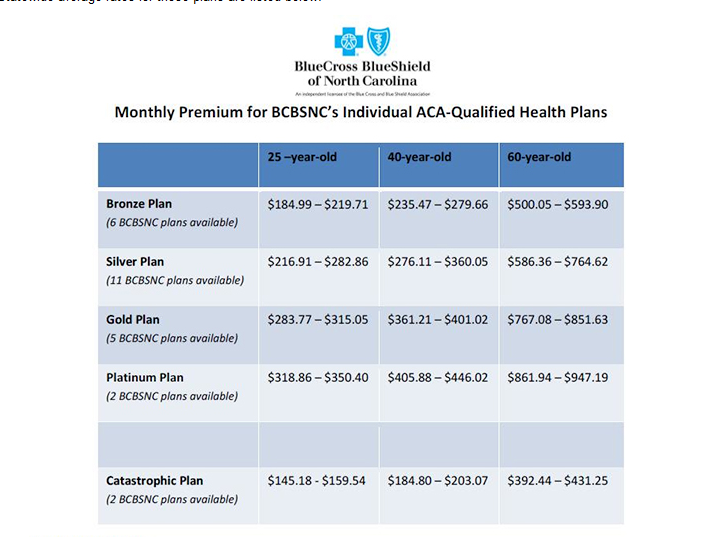

The big news this week is that actual pricing is starting to be released in a variety of states. The Reality Based Community passes along the fact that Blue Cross and Blue Shield of NorthCarolina released rates on everything they are offering on the North Carolina exchange/marketplace.

{kind=link}

(Click to embiggen)

There is massive variance in non-subsidized costs. The cheapest is $145 for catastrophic coverage for a 25 year old while the most expensive is a platinum plan for a 60 year old at $947 per month. Even looking within a single level for a single age, there are significant differences in price.

What are the factors that drive these cost differences?

The biggest drive of differential within the same plan is age. PPACA allows for up to a difference of 300% between the premiums for the youngest person who can buy a plan on the Exchange to a 64.999 year old. Age is an extremely good single predictor of medical expenses because as we get older, more things break down and recovery time gets longer. Late teens and early 20 somethings tend not to have too many chronic conditions nor do they fall and can’t get up. Furthermore, this age group just tends not to use basic medical services as much as they should. A 62 year old’s body has started to break down more often than my 1977 Chevy Nova plus by that point, most people have at least a chronic condition of some sort.

The next differential driver is the actuarial level of coverage. Catastrophic coverage is true “hit by a bus” insurance where the insurance only kicks in when a massive medical event occurs. It won’t help someone who has a clean broken leg, or needs an appendectomy or has an non-complicated pregnancy. Catastrophic coverage is available on the Exchange for people under the age of 30, as well as people whose employers offer insurance but it is not deemed affordable insurance.

The vast majority of people will buy a “metallic” product. Bronze has the lowest actuarial value at 60% while Platinum plans cover 90% of the expected average health care expenses of members. The higher the actuarial value of the product that a person buys, the more the insurance company is on the hook, and thus the higher a premium the insurance company charges to cover their anticipated cost. Doing some back of the envelope calculations, there is minimal pricing differentials within the lowest price metallic levels based on anticipated adverse selection usage rates. I don’t have their models in front of me to say for sure, but if there is adverse selection pricing, it is in the range of a good burrito to a decent lunch per month between levels.

Now within the Bronze plan for the 25 year old, there are six different plans being offered and their pricing is different. There are two major drivers of the differentials. The first is location. Typically community hospital and individual provider pricing is cheapest in the inner ring suburbs of a major metropolitan area as there is significant competition and comparatively cheap land. Within the anchor city of a metropolitan area like Charlotte, the basic hospital services and specialist services are a bit more expensive as the city is just more expensive. Charolotte would also typically host most if not all of the very high end specialty services (transplants, high end trauma centers, high end cancer centers). And once you get out into the boonies, pricing goes up again as there are very few providers out there. So location will drive some premium pricing as someone living in the local burbs is cheaper to cover than someone living in the center city or the boonies.

Within a single level, the location of the buyer matters to some degree, but the more important provider network driver of differences will be the type of network selected. I am betting that BCBS of North Carolina is offering a full network and a narrow network. The full network will be effectively a clone of one of their current networks with a new marketing name on top of it. The providers in the new full network will get paid commercial or near commercial rates.

The cheaper, but much more limited narrow network is a network that might have 50% of the doctors and 30% of the hospitals (including all of the high end services). The reason why it is a cheaper network is that the insurance company can got to five provider groups whose current rate structures are based on Medicare and the following multiples: 150%, 148%, 127%, 165% and 150% and make the following pitch: “We project that we’ll have 10,000 new patients in your area who are willing to travel for services, we’re paying 115% of Medicare, and we only need two of you… so who wants in?”

There is one other factor that can increase the cost of a plan. Tobacco usage allows an insurance company to apply a 50% surcharge on their age/location adjusted base rate for a given plan.

To review, in descending order of cost drivers for the exchange plans are the following:

- Age

- Value of plan

- Network breadth

- Buyer location

- Tobacco usage

There are a couple of important things that are no longer being considered in pricing policies. The biggest one is gender. Men tend to be cheaper than women from the insurance company perspective because men tend to use far fewer services (even when they should) and we can’t get pregnant. This fact is where the whining about the disadvantaged 23 year old male who is making $45,000 a year without employer/group sponsored health insurance and now he is getting screwed argument comes from. Yes, he is getting screwed because he is actuarially dirt cheap to cover but is now paying into covering everyone else.

The other big thing is health condition is no longer being considered. This how community rating is implemented. Everyone gets access to the same health insurance at the same rate structure. A thirty something diabetic epiletic can now get coverage on the individual market; previously that person would have been underwritten out of the market. So yes, the young triathelete is subsidizing their twin brother who weighs 400 pounds and is hypertensive, but that is any insurance scheme where the healthy subsidize the unhealthy. There are other systems in place in Obamacare to try and get those with controllable risk factors under control.

Chyron HR

As of this moment, I really, really can’t.

Richard Mayhew

@Chyron HR: give me a minute to get a better picture then :)

raven

Please explain:

jayackroyd

Can we just get a link to the NC Exchange? So we can see what a 25 year old gets for 1700 dollars a year? Because I think it’s probably better to roll the dice and rely on Medicaid for catastrophic coverage.

Ash Can

Great info. Once again, it’s a clearly imperfect system, but still far preferable to the just-plain-bupkis we had before.

jayackroyd

Here’s the reg I think. From http://bit.ly/184v5Zq

I’ll post it, then read it. (It is fabulous having a forum to discuss the nitty gritty. Thanks Richard!!)

Richard Mayhew

@raven: I don’t have the the details in front of me, but most likely there are three points being made:

1) $20.6 million dollars in additional mandated benefits — this is what it costs to keep kids on to age 26, this is what it costs to provide maternity care and other newly defined essential benefits that under previous plans were either not included at all, or included after a massive co-pay.

2) 8,400 people who either need to get insurance through their employer, a significant other’s employer or on the Exchange if the insurance being offered through the group market is deemed “unaffordable” OR pay the mandate penalty.

3) The back end of the new exchange markets has signifcant cross-subsidies so if Insurer A picks up a massive number of cardiac rehab patients, the rest of the system sends extra money to Insurer A to cover the risk. The goal here is to prevent an incentive for insurance companies to compete on who best can be unnattractive to sick people. The big goal of the exchanges is to create an insurance market where the insurers now compete on price, and quality instead of competing on dodging risk.

raven

@Richard Mayhew: Thanks!

Richard Mayhew

@jayackroyd: Jay — I don’t think the Federally run exchanges with full pricing are live yet.

The basic plan design for a Bronze level plan is something like the following:

$2500 to $300 deductible

20% co-insurance on the next $30,000 of expenses

co-pays of $25 to $50 for sick PCP visits and $50 to $100 for specialists.

There will be variance between carriers, but that is a generic general outline of what is needed to get only 60% actuarial value — and it is way better than running naked and getting hit by a bus.

Richard Mayhew

$2500 to $3000 deductible… not $300 deductible (that would most likely be a platinum plan design)

jayackroyd

OK, you get three primary care visits. Otherwise you’re out of pocket $6,000 before any insurance kicks in.

What makes this hideous to figure out is provider pricing is so insane, especially for any kind of inpatient visit. Are there clinics where you can get a checkup and followup with a primary care doc for less than $200 a visit? If so, I think you’re better off saving the premium and rolling the dice. Probably best to stash any savings with your parents or somewhere else Medicaid can’t see it. Or put it into your car, which you sell when you get hit by the bus so you can qualify for Medicaid.

I suppose this demonstrates the real reason the program needs an individual mandate. People under 35 or so in the bottom three quintiles are gonna get whacked pretty hard if they participate.

jayackroyd

Thanks Richard. Lemme get out my envelope….

Sorry, meant to ask whether that link I posted from the NCSL is a useful guide.

gene108

Any info on what annual out-of-pocket max’s will be for these plan in Year 1 of Obamacare?

I heard the 6k single/12k family out-of-pocket max structure got pushed back by a year.

The only way co-insurance works for an individual is to have out-of-pocket maximums or some sort of stop-loss provision, either in aggregate or due to a specific event, because at some point reinsurance would kick in for the insurance carrier and the carrier no longer directly be on the hook for covering claims.

jayackroyd

@Richard Mayhew: Are there copays on well PCP visits? I assume at least two are covered, as women generally have two primary care relationships. (Actually, I figured that’s where “three” came from in the State legislature summary. Two well care visits, plus one followup.)

Also I wasn’t asking about the federal exchanges. I was asking about the NC BC options. Are those not online? Your chart seems to come from an AP story that’s probably based on a BC press release.

WereBear

Well, sure… if you don’t really need that leg.

Being insured means you get an actual doctor and something of an evaluation and treatment plan, right away.

Screwing around with losing your assets and wading through the voluminous paperwork, especially in a case where you are expected to have insurance, means your life will be saved, but your quality of life is definitely up for grabs.

jayackroyd

@Richard Mayhew: On running naked, if you’re hit by a bus running naked, you sell your assets, pay off as much as you can and go to Medicaid.

That’s why I’m a little confused about why anyone would buy catastrophic coverage. Medicaid is the insurer of last resort. Unless you have assets greater than the catastrophic out of pocket costs before everything is covered, it’s crazy to buy catastrophic coverage.

Now this doesn’t apply to top two quintile people in their 50s of course–they essentially have to declare bankruptcy to qualify for Medicaid. But for someone under 30 with a negative net worth, I don’t see what a catastrophic plan does for her.

gene108

@jayackroyd:

Preventive care, i.e. annual check-ups for example, are free under Obamacare.

Also, when you are part of an insurance network, even though you pay everything until you hit the deductible, you still get the benefit of the insurance network discounts.

So you go to the hospital. The cash payer bill is $2,000, but because you have insurance and get insurance network discounts that apply to the provider, you only pay $1,000. It’s not perfect but you can recover the cost of receiving care versus what you pay in premiums, with these discounts even before you hit your deductible.

Christie, here in NJ, dropped the income requirements for qualifying for Medicaid from 25k a year to 5k a year. The amount you’d have to stash to qualify for Medicaid not only varies from state to state, but will vary based on who is in charge of the state government and the kind of changes they make to the plan.

You may be good hiding your money one day, but the laws can change and unless you decide to live under a bridge, there’s no way to hide enough money to qualify.

Yes the mandate is needed to keep people for signing up for insurance right before they need surgery, but this goes for a lot of demographic groups.

You could have a 50 year old uninsured man, who needs may need a heart operation, that avoids getting insurance until right before going for surgery because he’d be able to save money on the premiums. That’s probably a bigger fear for insurance providers than a 22 year old guy not opting for insurance until right before needing some kind of surgery.

The 22 year old probably is not putting off any major procedures and by the time the 22 year old gets hit by a bus and needs insurance, it’ll be too late to sign up in advance because by the time the 22 year old wakes up he’s already had the ambulance rush him to the ER and has had a stay in the hospital.

Richard Mayhew

@jayackroyd: @gene108: No cost sharing for wellness visits (for me — that is just the annual PCP, for my wife, annual PCP and annual Ob/gyn, for Kid #1, annual pediatrician and vaccines, Kid #2, multiple pediatrician and vaccine visits)

Cost sharing (co-pays and deductibles and co-insurance) allowed for PCP visits that are sick visits — so if my youngest has the croup, we’re paying something to get him care.

As far as the North Carolina exchange, it is not up yet, so there are no comparisons to see how the rest of NC is pricing out. I played around with the North Carolina BCBS website, and their exchange plans don’t seem to be displaying yet either (I could be wrong). So yes, I’m using a press release for illustrative purposes.

jayackroyd

@WereBear: I’m not sure what scenario you’re thinking of here. If you’re hit by a bus they treat you, then figure out how to get paid.

On the other hand, I agree with your larger point–that most people are happy to pay for the assurance that they can hand over an insurance card and not have to worry about anything other than getting treated. It’s one reason I don’t actually believe in adverse selection being an important issue–and that all the complex group constructions that the insurance companies say are needed to prevent adverse selection are there for a different reason.

Continuing on that tangent, one good thing the ACA does is eliminate these crazy one or two person groups that were gouging people.

jayackroyd

@Richard Mayhew: Thanks. And thanks again for posting this thread.

Richard Mayhew

@jayackroyd: Real simple — keeps them from declaring bankruptcy.

A while ago, I was in my mid-20s and out of work. I bought a catastrophic policy with a $7500 deductible and a $15,000 OOP max for myself because I figured that if I was hit by a bus/came down with cancer etc, I could over the course of a couple of years come up with $15,000 while getting good care but there was no way in hell I could dig out of a $250,000 hole or a $30,000 hole after a bankruptcy settlement while dealing with bankruptcy.

WereBear

@jayackroyd: Yes, they treat you.

But they have wildly varying ways to do that, and if you need a topnotch protocol that starts right away to get the best outcome… they don’t dive into that for someone who doesn’t have insurance. There are waiting lists at good rehabilitation centers for people who get right into the system. Screwing around adds delays at a time when you really are throwing dice, more than you know.

We are talking catastrophic here, and I know what that means. It means ten years ago, you probably wouldn’t make it. Now, you will, but it involves a very long road back and a possible continuum from “good as new” to “head in a jar.”

You don’t seem to realize what you are really gambling with under this scenario.

WereBear

@Richard Mayhew: This, too, excellent point.

Jiminy Christmas, I had my husband die, my business go under, and my house yanked away, and I still had to save up enough money to declare bankruptcy.

jayackroyd

@gene108: Thanks Gene. I don’t actually believe in the 50 something who stays out of the system until he needs major surgery scenario. I think that’s one of the insurance company’s adverse selection fantasy stories.

The real issue is, as you’re saying implicitly, is finding a way to use private insurance to do the life cycle equalization that you get for free from a single payer or socialized system. The period of time of lowest health risk coincides with the period of lowest income. It’s not impossible to do this; that’s how the systems work in Germany or Switzerland. But they operate with a great deal more transparency of provide pricing and, non-profit private insurance that is strictly regulated.

In the short run, compliance with the individual mandate for the under 30 cohort will be a problem. $1700 is a lot to pay for three well visits.

jayackroyd

@Richard Mayhew: Again, I’m confused. You apply for Medicaid in such a scenario.

jayackroyd

@WereBear: We’re not talking about me. ( I really don’t understand why these things go all ad hominem so quickly.)

We’re talking about the bottom three quintiles (in income) of people who are under 30. That’s the uninsured population you need to bring in to compensate the insurance stakeholders/rentiers for cutting their medical expense ratio and not disallowing people for pre existing conditions.

It seems to me that asking someone like that, currently running naked, to pay out 1500 dollars a year in order to receive three well visits and the privilege of paying out another 3-6K before any coverage kicks in, is asking a lot.

Freemark

@jayackroyd: It is not 1500-2000 a year for almost any -29 year old. If you are <30 you are probably making less than $45,000 a year. Which means it is subsidized to some extent. For example if they make $25,000 a year the cost would be more like 2-300 per year at most, probably less. If they are making more than $45,000 than the idea of going on medicaid really makes no sense and they probably have an employer option to boot.

WereBear

I wasn’t implying you were stupid or anything; you brought up excellent questions and I was trying to bring up others.

Aren’t there subsidies for low income folks in any case? I don’t believe the online calculators consider that, which makes a huge difference.

gene108

@jayackroyd:

Hoping this Obamacre v. 1.0 will lead to more transparent pricing standards in the future. I look at this law as the first step on a long road to a better health care system.

sparrow

@jayackroyd: Is it really asking a lot? Maybe if they are stupid. I’ve only recently exited my 20s, but I was dirt poor for most of them and I definitely ponied up the cash for catastrophic health insurance when I went off my school’s plan. It was kind of in the “basic life expense that must be paid” category, along with rent and utilities. I would eat beans and rice to pay that bill. And I’m super healthy, and not particularly risk-averse. But I’ve always known that no insurance is a bad, bad road to be on if something goes wrong.

Richard Mayhew

@jayackroyd:

Under 30 bottom quntile is MA eligible if the state took up MA expansion.

2nd quintile, an individual is either going catastrophic coverage or Bronze plan with very significant subsidy so monthly premium costs are $30 to $50 a month

3rd quintile is the iffy case

Steve

Even though there’s no more gender discrimination in pricing, there’s probably a big gender gap in who will buy the catastrophic policies, the ones where the deductible is too high to cover the cost of a normal pregnancy. If you’re a young, healthy woman who plans on getting pregnant or thinks she might, a policy like that won’t be a good option for you, while it might be a reasonable option for a healthy man of the same age.

So we don’t have gender rating any more, only we sorta do because men and women are buying different entirely different products now. I don’t know if this is a big problem – I guess maybe it depends on how many men are actually going to go with the catastrophic care option.

By the way, I haven’t been around much lately, I’m curious if “Richard Mayhew” is a new front-pager or an old one under a new pseudonym. Great posts either way.

Richard Mayhew

@Steve: New guy

TaMara (BHF)

I’m very glad you’re here to do this. There are going to be a lot of questions as this goes forward. I know I was really, really cranky when Colorado’s plan prices became available. Still crabby about it but will wait to see as it gets closer, to what that really means.

Steve

@Richard Mayhew: Welcome, new guy! It’s a funny coincidence because I just finished reading that book last week.

the Conster

The HSAs are funded with pre-tax dollars and it’s your money and it accumulates all the time it’s not being used. A lot of employers match or subsidize the deductible amounts too, and it can be used for dental care and eye care which is great.

Richard Mayhew

@TaMara (BHF): Your crankiness was actually one of the reasons why I wanted to write this series

Aurona

Speaking as a senior who worked at BC and BS in California before moving northward to Washington, looking at the rates are one thing, as Richard points out, and receiving the subsidies are another. If I could have gotten ACA when I retired at 62, I would have been in hog heaven. With rates based on my income, I could have had a nice little policy to tide me over until Medicare kicked in and gotten preventive care; and don’t forget Rx is included on this (varies with the policy offered, I am sure). This is a great policy for the 50-64.99 set; the kids who are not making much money in their 20s will not feel a huge burden, as it is still much cheaper and better coverage (preventive care/prescription drugs) than was offered the last few years. Of course, your mileage will vary in the state you live in, but its a good start toward Medicare For All.

Also, Too: Thank you Richard for posting. Keep it up!

jayackroyd

@Freemark: Right, it’s the subsidy that will make this work. And, yes if coverage is under 500 dollars out of pocket for an <40K earner, I think most people weuld take it. It's not a fair bet, but it's worth the peace of mind (I still don't believe in adverse selection.)

askew

@Steve:

A lot of the exams for pregnancy are covered at 100% for preventive care I believe. I think the actual delivery is still not covered at 100% though.

jayackroyd

@gene108: Yes, that’s the glass half full viewpoint. There are elements of ACA that support that optimism. Talking to RJ Eskow last night, he says that the guys working in the claims depts will find ways to game this; it’s their job. ( http://bit.ly/184URgl )

TaMara (BHF)

@Richard Mayhew: It’s nice to know that being bitchy has a purpose. LOL.

gogol's wife

Boy, I really don’t have time to read these threads, but the fact that they exist is fantastic! This is a real public service by Balloon Juice.

ETA: And of course thanks to Richard Mayhew.

Stella B.

,@jayackroyd:the only way you get out of paying the bills you rack up by being uninsured is through declaring bankruptcy. Then your credit rating is toast andyou can’t buy a car or a condo and you’ll probably have trouble getting a job or renting an apartment. If you are a young person just starting out that probably translates to a lifetime of reduced earnings.

Mnemosyne (iPhone)

@jayackroyd:

You keep saying “$1700 a year,” but I think most people would look at the monthly cost, which is about $141 per month. That doesn’t really seem like a crazy expense to me — a lot of people pay that for their cell phone or cable bill. It’s definitely much less than a car payment. And once you take the subsidies into account, it will be much less than that for most of the under-30s.

Irony Abounds

I’m 58, and currently have an individual policy that covers myself and my 19 yr. old daughter for around $300 a month. It’s an HSA, with a $10K deductible. I haven’t seen any numbers out of Arizona yet, but I have a feeling that my premium is about double, based on the numbers that I have seen on the Bronze plans around the country. I understand the reasoning for community rating, but I think it is a mistake to eliminate virtually all incentives for maintaining good health (or conversely, eliminating virtually all disincentives for making healthy choices).

Given the subsidies that are in place, I would prefer to make those who can afford it and have made bad health choices and therefore utilize the system more at least pay a bit more than those who make better choices. At least smokers get hit for being moronic twits for smoking.

Pamoya

MN Sure, the exchange in Minnesota, released some info on plan pricing on Friday. Unfortunately, it’s all “averages” and I can’t figure out what the heck that means, especially since some of the averages have ranges. (Yes I understand the usual definition of average.) On the bright side, the premiums look pretty low to me, though I can’t tell what the deductibles will be.

Any ideas how the new system fits in with Health Savings Accounts? Can you still use an HSA if the plan you pick has an approximately $1500 deductible or higher? Would this limit you to a bronze plan or something? Correct me if I’m wrong, but is it true that bronze/silver/gold does not denote anything better or worse about what kinds of things are covered, but are only about how much of the cost your premium payment covers?

Mary

@jayackroyd: seems to me these guys are already covered. I mean, why wait to apply for Medicaid after you’re hit by a bus? Get it before you get creamed if your eligible. If you’re not, then you should be eligible for a subsidy that will net you price no where near $1700.

The only gap in coverage is in states without the Medicaid expansion. In those states, there’s a donut hole of single people who make too much to qualify for Medicaid, but also don’t make enough (approx. $16,000) to qualify for a subsidy either. Those are the folks, like me, who will pay the penalty and wait for a catastrophic emergency to apply for a policy through the exchange.

Richard Mayhew

@Pamoya:

“Correct me if I’m wrong, but is it true that bronze/silver/gold does not denote anything better or worse about what kinds of things are covered, but are only about how much of the cost your premium payment covers? ”

Correct, the metal names just signify what % of actuarial cost the insurance company pays for. It does not describe benefit configuration or networks.

Steve

@Irony Abounds: I think it’s a mistake to look at health care costs as the major disincentive for unhealthy behavior, as I think your statement “it is a mistake to eliminate virtually all incentives for maintaining good health” would imply.

The major incentive for healthy behavior is to remain healthy. Even if it’s completely free, people don’t like getting sick, developing health problems, going to the doctor, having surgery, etc. Nobody says “oh well, who cares if I have a stroke since it’s covered by insurance.” And even though, for example, bad diet is correlated with obesity which is correlated with various health problems, we shouldn’t overestimate the volume of health problems that are easily “preventable.” To the extent monetary incentives even matter in the first place, only a small part of the health care universe will be impacted.

Ted & Hellen

Jesus Christ.

The average person should not have to hire a team of lawyers and medical advisers, which they can’t afford in the first place, to figure out which one of these incredibly complicated plans they should buy. It’s (fucking!) ridiculous. The average person’s eyes glaze over looking at this barrage of options, they throw up their hands or do their best to pick something that feels like it might do some good, and underneath it all is the abiding suspicion that they are being screwed by the medical industry and the insurance industry and the government. And they’re correct.

The exchanges mostly appear to be a bureaucrats’ dream of job security.

What a load of crap.

If only Obama could have been bothered to launch and maintain a full press, 24/7, months long, all out push for Single Payer to equal his campaign to get his war dick on in Syria. (But the bully pulpit doesn’t work!)

Utter transparent bullshit.

JGabriel

@Richard Mayhew: … it is way better than running naked and getting hit by a bus.

#streakersplat

Manyakitty

So, this morning at work, my boss handed out a couple of pages about insurance options and said that we need to sign up for the exchanges because our employer-based coverage will stop as of January. Ohio’s participation has been sketchy at best, and now we (three employees) are very confused. Should we just hang on until the exchanges open in October or what? He also said that he plans to increase our wages by approximately what we’ll pay, but I can’t see how any of us will pay the same rate, so some of us will get a smaller increase than others. ARGH.

Stella B.

@jayackroyd: also, too, there’s an enrollment period. So get hit by a bus in April and wait until December to buy coverage? Probably not a good plan.

richard mayhew

@Ted & Hellen: So you believe in Green Lanternism and the power of the Bully Pulpit when the critical votes in 2009 are Senators Lieberman (I-Insurance Industry), Landrieu, Pryor, Begich in the Seante and in the House the key votes are from Dems representating R+5 or more districts…

Tell me how you get 218/51 (much less 60) with good speechifying

richard mayhew

@richard mayhew: Institutional design matters. If Obama wanted to launch cruise missiles three weeks ago, there are no veto points in the American political process from that happening (see Grenada, see Panama, see Desert Fox, see ’98 cruise missiles into Sudan and Afghanistan, see drones in Yemen) Sustained presence and operations run into War Power Act constraints, and Obama asking for an AUMF from Congress is a self-imposed constraint that looks like it will prevent him from, as you put it, getting his war on.

Now making systemic changes to a major sector of the American economy and the American citizen relationship with government is rife with veto points. The entire process favors doing nothing, or doing something that involves buying out impacted interests. Major speechifying and a full court press on veto actors who either are indifferent to the change or are actively opposed to that change leads to failure (see Bush in 2005 with Social Security privatization — he bully pulpited the living shit out of the proposal and never even got draft legislatiton out of committee because the Republicans in Congress, (rightfully) feared for their jobs if they killed SS and let everyone know about it)

Sure, I agree with you and Jay that single payer is more effective and more efficient in a world where policy is made behind a veil of ignorance and there are no pre-exisiting interests or institutional veto points. But we don’t live in that world. The relevant question for a world of second bests is what is the counterfactual and is the policy change better than the status quo in the counterfactual. MA expansion and Exchange is a massive improvement over the counterfactual of doing nothing or doing a small CHIP expansion.

Mnemosyne

@Manyakitty:

There are apparently a couple of advocacy groups in Ohio that are trying to do the job that your governor is refusing to do: Protect Your Care and Americans United for Change. You may want to see if you can reach them and get some answers.

I know that here in California, state advocates are going all over to educate people on their options. They were even advertising one meeting at my local knitting shop. So you may want to see if any of the small businesses you frequent are stepping up to help consumers out.

Irony Abounds

@Steve: I think you underestimate the costs of an unhealthy lifestyle, and overestimate the incentive of “being healthy” (if it were really a big incentive you wouldn’t have so many people who overeat, smoke and/or drink too much). I just have a problem with a community rating system that does not have any reward for those in good health who will be much less of a drain on the system than those who are not. As long as a system of subsidies is in place, I think it is helpful to the system as a whole to create incentives for a healthy lifestyle.

Manyakitty

@Mnemosyne: THANK YOU! I’ll get their contact info and share it with my co-workers.

Mike E

Not to tag onto a dead thread, but this timing is perfect for me: I turn 50 soon, and I am “in the market” looking for heath ins which I don’t currently have (long story, but I’m sure you already know it). I’d hate to echo T&H about “this shit is fucked up and bullshit” (we should have 2-way wrist radios & The Jetson’s hovercars too!1!) but we are where we are and I need to take care of myself, and like I said, the timing is perfect.

I currently work several p/t jobs tho one could become a semi-permanent position (city! Hurray!). My salary is < 18,000. I may qualify for MA, but I am also curious what "metal" I should get from BCBS. Any advice would be greatly appreciated.

ETA Oh, I’m in NC btw, and poor!

muddy

@Ted & Hellen:

Even if that were so we don’t have a time machine. We go forward from here, there’s nothing to be done about that.

Ted & Hellen

@muddy:

Look forward, not back?

There are always lessons to be learned from past performance, yes?

Mike E

@muddy: How do you know PBO doesn’t have one? ;-)

muddy

@Ted & Hellen: You aren’t giving any lessons learned or saying how to go forward. You just keep saying how he didn’t do it right before.

It’s the banging the head on the wall thing again. I don’t know why you torture yourself so.

muddy

@Mike E: I was just presuming from previous experience? Anyway, all this talk about the war dick spinning about over our heads (oh that’s from the further thread, but anyhow..) is giving me a distressing visual of the prez as some kind of bizarre helicopter.

It will give me a nightmare.

Mike E

@muddy: He’s all things to some people, if’n you know what I mean.

muddy

@Mike E: Ayup.

richard mayhew

@Mike E: @Mike E:

Okay, I am not a licensed insurance agent — here is what I would do:

1) See if you are MA qualified (probably not as NC is not a MA expansion state)

2) Wait until October 1 and do a long recon of the exchange site and figure out what is available to you where you live.

Subsidies are based on the 2nd cheapest Silver Plan and are on a sliding scale based on income. Due to your income, you’ll probably get a very significant subsidy.

3) Figure out your current health status and your ability to absorb a loss and your ability to pay each month.

The rule of thumb is the more you can’t afford a big loss/deductible payment, the shinier the metal you should get. Now what does that mean for premiums and your budget, I don’t know.

richard mayhew

Furthermore, don’t buy October 1 — wait a couple of weeks to really figure out what you feel comfortable with given your options… if anything wait as long as you can so that you get the new information of your December health status instead of your October health situation….

Manyakitty

@richard mayhew: Based on my discussion with a live chat agent at healthcare.gov this morning, for coverage to start on January 1, 2014, the insurer needs the first premium payment by December 15, 2013. Assuming administrative lag, I’m not sure waiting until December is a good idea. Frankly, I still wish my employers decided to take advantage of the delay for small businesses, if for no other reason than I’d rather the bugs get worked out before I’m forced into the fray.

Mike E

@richard mayhew: Awesome, thanks. I am strong like bull (best read with Rooshian accent), don’t visit drs much, and can wait. Whenever I have visited a physician friend of mine, he kinda shakes his head and thinks to himself, “what hypochondriac thing are you wasting my time with now?” When I turn 50 tho, all bets are off.

richard mayhew

@Manyakitty: than go shopping around Black Friday for health insurance — one thing insurance companies are good at is depositing money in the bank quickly

Manyakitty

@richard mayhew: Fair enough. Thanks!

pseudonymous in nc

For once, I’m with Ted & Hellen on the basic principle: these are options designed for bad choices. And yeah, yeah, the votes weren’t there, and there’s going to be education in the coming months, but how damn inefficient is that? It’s like buying mattresses. The illusion of choice.

The NC state employee plan has just three options: an 80/20, a 70/30 (grandfathered) and a HDHP/HSA “consumer driven” plan. (And I remain unconvinced that HDHP/HSAs aren’t fundamentally bullshit.) You’re still going to get screwed one way or another depending on what you choose, so it’s a guess as to whether you pick the one that screws you the least during the coming year.

J R in WV

Here’s a scenario. Spouse on total disability, receiving social security, under 65. Former employer in financial trouble has provided medi-gap insurance that covers substantial prescription costs to treat her total disability.

Employer plans to end current health care insurance plans as of 12/31/2013, replacing insurance with flat $1700 annual payment IF spouse selects one of their pre-approved insurance plans. Actual content of pre-approved plans still SECRET making planning very difficult!!

What’s the best option under the new healthcare insurance regime?

Medicare Plan D for the necessary drugs? What about the famous donut hole?

I know this thread is dead, but if anyone who knows anything about these issues could pitch in I would be very grateful!

Thanks for all the valuable information these updates are providing!

Richard Mayhew

@jayackroyd: Jay if you do not believe in adverse selection, please explain the New York State individual insurance market pricing with community rating but no risk pool management system like a mandate

Richard Mayhew

@J R in WV: donut hole is shrinking to zero in next couple of years… other than this speak with a local broker and pay them a flat fee for an hour of their time and buy fro m someone else

Stuart Zechman

@Richard Mayhew:

“if you do not believe in adverse selection, please explain the New York State individual insurance market pricing with community rating but no risk pool management system like a mandate”

That’s fairly simple to explain: the NY State insurance industry raised its prices 20% to 50% almost overnight. In one month (March, 1993), after community rating/guaranteed issue regulations became law, the average annual insurance premium in New York State for a single male aged 30 rocketed from $1,200 to $3,240.

That’s not some natural force at work, that’s a cartel of price-fixers imposing collective punishment on the population of New York for the crime of regulating them.

The idea that the solution to the price fixing is anything other than destroying that industry’s capacity to create markets is bizarre, unless one sees that industry as integral to the rational pricing of health care, and the involuntary transformation of that industry into a form of public sector utility as Soviet-style governance.